.webp)

Credit Card Refinancing vs. Debt Consolidation

Credit card debt is on the rise among households across the country. According to the Federal Reserve Bank of New York report from the second quarter of 2023, total credit card balances topped $1 trillion for the first time. More people are also falling behind on credit card bills—perhaps, in part, because credit card interest rates have steadily increased over the last year.

If you’re looking for a strategic way to make the best out of a tough financial situation, refinancing and consolidating credit card debt might be a solution.

Credit card refinancing and debt consolidation: two sides of the same coin

Credit card debt consolidation is when you use a new loan or line of credit to pay off two or more credit card balances. Consolidating your debt doesn’t save you money right away. In fact, upfront fees might increase the total amount you owe. However, it can make paying off your debt easier and might save you money in the long run.

Refinancing is when you take out a new debt and use the funds to pay off an existing debt. You can benefit from refinancing if the new debt has more favorable terms, such as a lower interest rate or lower monthly payment.

People generally refinance credit card debt with either a personal loan or a balance transfer credit card with a low introductory rate. And because they often use the loan or balance transfer credit card to pay off several credit card balances, they’re refinancing and consolidating their credit card debt at the same time.

Benefits of credit card refinancing

Consolidating and refinancing credit cards can offer several benefits that could help you get out of debt.

- Fewer payments: It can be easier to focus on a single monthly payment than dealing with multiple payments throughout the month.

- Lower monthly payments: Your monthly payment on the new loan or credit card may be lower than your current combined minimum payments.

- Interest savings: You might qualify for a lower-rate loan or a 0% balance transfer offer and can put the interest savings toward paying down the debt faster or covering other expenses.

- Might help your credit score: Consolidating credit card debt can lower your credit utilization ratio, which can build your credit.

Drawbacks of credit card refinancing

However, you’ll want to consider the drawbacks and other credit card payoff strategies to determine if refinancing makes sense right now.

- Might require good credit: It can be difficult to qualify for a low-rate loan or a credit card with a high transfer limit unless you have a good credit score.

- Fees can limit your savings: Loans may have origination fees and credit cards may have balance transfer fees. These upfront fees can eat into the potential savings that come from having a lower interest rate.

- Doesn’t address overspending: Consolidating the debt and freeing up your credit limits won’t address the root issue if you have credit card debt due to overspending. You may wind up with a new loan and slowly rack up credit card debt again.

How to consolidate and refinance credit card debt

There are two popular options for consolidating credit card debt—personal loans and balance transfer credit cards.

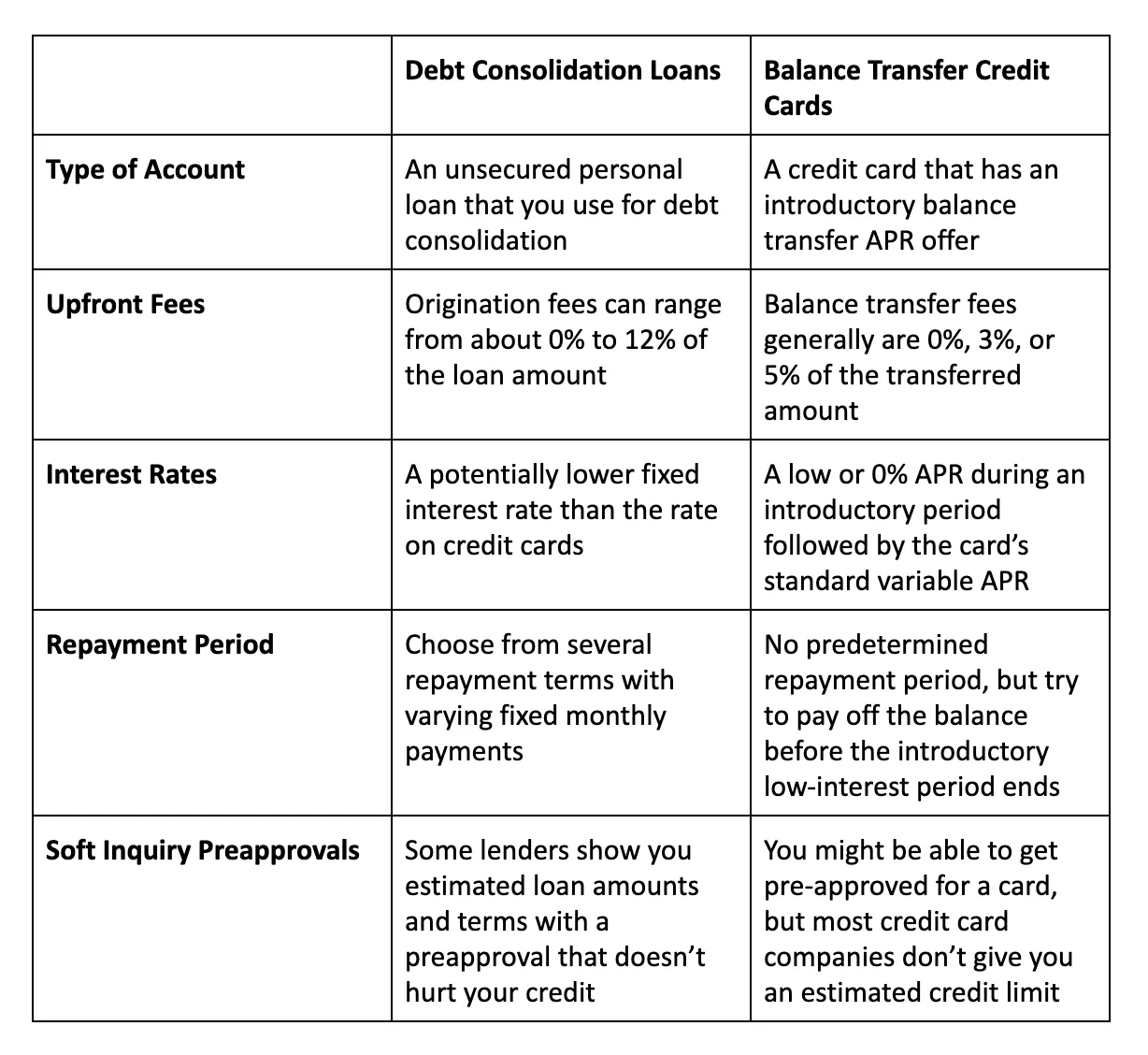

How to consolidate debt with a personal loan

A personal loan is an unsecured installment loan. When you apply, the lender may consider your credit history, credit score, income, and outstanding debts and, if you’re approved, give you several loan offers.

You can generally choose from a few repayment loan terms, such as three or five years, and each has a corresponding interest rate and monthly payment. If you get an offer with a lower rate than your credit cards’ APRs, consolidating with a personal loan might make sense.

Once you accept a loan offer, the lender will send you the funds and you can use them to pay down or pay off your credit card balances. Alternatively, some lenders can send the loan’s proceeds directly to the credit card companies.

How to consolidate debt with a balance transfer card

A balance transfer credit card is a regular credit card that has an introductory balance transfer offer.

For example, you might receive a promotional 0% APR on balances that you transfer to the credit card. If you transfer high-interest credit card debt, you’ll accrue less interest and you’ll have more money to pay down the balance.

You may be able to request the transfers when you apply, or log into your new credit card account and request a transfer once you receive your new card. But don’t delay. Generally, the promotional rate only applies to balances that you transfer within a certain time, such as the first 60 days. Also, you often can’t transfer balances between cards from the same issuer.

The terms and promotional periods depend on current card offers, with some of the best options offering 0% APRs on balance transfers for over 20 months. Any balance remaining on the card at the end of the promotional period will start to accrue interest at the card's standard interest rate.

Personal loans vs. balance transfer cards: which option is right for you?

Final tips and thoughts

Consolidating and refinancing credit card debt might lower your interest rate, decreasing how much interest accrues and freeing up money to pay down balances faster.

However, no matter which method you use, continue monitoring your credit cards’ balances for a couple of months. Sometimes residual interest can accrue and lead to one final bill after you pay off or transfer your balance. Even missing a payment for a few dollars of interest could result in late payment fees and hurt your credit.