Purchasing a car is often one of the largest financial decisions people make outside of buying a home. Whether you're purchasing your first vehicle, upgrading, or replacing an older car, understanding your financing options is key to making the smartest choice for your wallet—and your long-term financial health.

Many buyers face the question: Should I finance my car through a bank, a dealership, or explore alternative lenders? This guide focuses on financing through a bank, breaking down the step-by-step process, benefits, potential drawbacks, and how your financing choice connects to your overall credit history.

If you're also working on building your credit profile, understanding how car loans impact your credit report—and how tools like Ava Finance can help support credit history improvement—can make a significant difference.

What Does It Mean to Finance a Car Through a Bank?

Financing a car through a bank means applying directly to a financial institution for an auto loan rather than using dealership-arranged financing. This approach often allows borrowers to:

- Compare multiple loan options

- Understand total borrowing costs upfront

- Potentially secure better interest rates, especially with strong credit history

- Negotiate with dealers as a "cash buyer," providing leverage during purchase discussions

When you finance through a bank, you receive the loan directly from the lender, who pays the dealer or seller, and you repay the bank through structured monthly installments.

Step-by-Step: How to Finance a Car Through a Bank

1. Check Your Credit History and Credit Standing

Before applying for an auto loan, it's essential to check your credit report and understand your credit standing. Lenders heavily consider your credit history when determining loan eligibility, interest rates, and loan terms.

Typically:

- Higher credit scores result in lower interest rates and better loan terms

- Lower credit scores may lead to higher rates or additional requirements like larger down payments

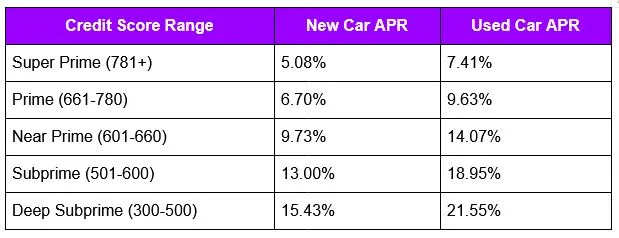

Average Auto Loan Interest Rates by Credit Tier (as of 2024):

If you're working on improving your credit history, tools like Ava Finance can help by reporting eligible rent, utility, and subscription payments to all three major credit bureaus¹, providing an opportunity to support positive credit history over time.

2. Get Preapproved for an Auto Loan

Preapproval provides insight into:

- The loan amount you qualify for

- Estimated interest rates

- Monthly payment estimates

Preapproval may require:

- A hard credit check, which could temporarily impact your credit profile

- Documentation like proof of income, identification, and other financial details

Benefits of preapproval include:

- Understanding your budget before shopping for a car

- Negotiating with dealers from a position of strength

- Comparing loan offers from multiple banks to secure favorable terms

Tip: Preapproval is typically valid for 30-60 days. Be ready to shop within that timeframe.

3. Shop for Your Vehicle

Once preapproved, explore different car options, considering:

- New vs. used models

- Manufacturer warranties

- Vehicle reliability and total cost of ownership

Dealerships may offer incentives, but with preapproved bank financing, you retain flexibility to negotiate the vehicle price independently from loan terms.

4. Gather Required Documentation for Bank Financing

When finalizing your bank loan, you'll need:

- Valid government-issued ID (e.g., driver’s license, passport)

- Social Security number for credit verification

- Proof of income (pay stubs, W-2 forms, bank statements)

- Proof of residence (utility bill, lease, or mortgage statement)

- Vehicle details: purchase price, VIN, year, make, and model

- Current vehicle title/registration if trading in an older car

- Proof of insurance meeting lender requirements

5. Finalize the Loan and Confirm Terms

Before signing your loan agreement:

- Review the interest rate, repayment term, and total loan cost

- Understand any fees or conditions

- Ensure monthly payments align with your budget

Upon approval, the bank disburses funds directly to the dealership or private seller, completing your vehicle purchase.

Bank Financing vs. Dealership Financing: What’s the Difference?

Bank Financing Advantages:

- Direct loan application with banks, credit unions, or online lenders

- Potential for competitive rates, especially with strong credit history

- Preapproval simplifies car shopping and negotiations

- More transparency over loan terms

Bank Financing Considerations:

- Loan approval may depend on knowing specific vehicle details

- Preapproval process may take longer than in-house dealership financing

- Borrowers need to independently research lenders and loan offers

Dealership Financing Options:

- Dealer-arranged financing through partner lenders

- Captive financing through the manufacturer's finance company (e.g., promotional 0% APR offers for qualified buyers)

- "Buy Here, Pay Here" financing for individuals with challenged credit (often higher rates and stricter terms)

While dealership financing can be convenient, buyers may have limited lender options, face potential APR markups, and lack negotiating leverage compared to preapproved bank financing.

Is Bank Financing Right for You?

Consider financing through a bank if:

- You want to shop for the most competitive loan rates

- You prefer to negotiate as a "cash buyer" with preapproved funds

- You're purchasing a vehicle privately, outside of a dealership

- You have strong credit or are actively working to improve your credit history

Dealership financing may suit you if:

- You qualify for promotional manufacturer financing offers

- You prefer convenience and dealer-managed loan applications

- Your credit is limited, and you need broader financing options

Loan Terms: How Long Will a Bank Finance a Car?

Auto loan terms vary, typically ranging from 12 to 96 months:

- Shorter terms (36-48 months) often carry lower interest rates but higher monthly payments

- Longer terms (72-96 months) offer lower payments but may include higher overall interest costs

Average Auto Loan Term: 72 months

Choosing the right term depends on balancing monthly affordability with minimizing total interest paid.

How Car Loans Impact Your Credit History

Auto loans, when managed responsibly, can support your credit history by:

- Diversifying your credit mix (installment loans and revolving credit)

- Establishing positive payment history with on-time monthly payments

However, late payments, delinquencies, or loan defaults can negatively affect your credit history.

Monitoring your credit report regularly can help you track how your car loan influences your financial profile. Services like Ava Finance offer credit monitoring tools and support resources to help users understand their credit history and manage their financial journey effectively.

How Ava Finance Supports Your Credit-Building Efforts

If you're financing a car and working to strengthen your credit history, Ava Finance offers tools designed to help you:

- Report eligible rent, utility, and subscription payments to all three major credit bureaus¹

- Monitor your credit report with alerts for changes

- Access educational resources to help you understand your credit history and work toward credit health goals

Important: Approval for Ava products like the Ava Credit Builder Card or Save and Build Account is not guaranteed. Successful bank account linking via Plaid is required, and failure to maintain this connection may result in product termination. Ava reports activity to all major credit bureaus, but specific credit outcomes are not guaranteed and may vary.

Explore full details and terms at meetava.com.

Conclusion: Drive Smarter with Informed Car Financing

Financing a car through a bank provides flexibility, transparency, and the opportunity to secure competitive loan terms, particularly for borrowers with strong or improving credit histories. By comparing loan offers, preparing required documents, and understanding the impact of financing decisions on your credit history, you can navigate the car-buying process with confidence.

As you manage your car loan and overall financial responsibilities, tools like Ava Finance can complement your efforts to build positive credit history, helping you work toward broader financial stability.

Visit meetava.com to learn more about resources designed to support your financial journey.