You work hard for your money—but that doesn’t always mean you get to access your earnings when you need them most. For millions of workers, waiting two weeks (or longer) for payday can make budgeting feel like a juggling act. Essential expenses like rent, utility bills, and loan payments don’t always line up neatly with your pay schedule, and unexpected costs—such as car repairs or medical bills—often arrive at the worst possible time.

This mismatch between when you earn money and when you receive it can lead to cash flow gaps. If left unmanaged, these gaps may force you into costly short-term solutions like payday loans, high-interest credit card cash advances, or late bill payments—all of which can damage your credit report and hold back your credit-building goals.

That’s where Earned Wage Access (EWA)—sometimes called on-demand pay or instant pay—can help. EWA allows you to withdraw a portion of the wages you’ve already earned before your scheduled payday. By doing so, you can better align your income with your expenses, pay bills on time, avoid late fees, and keep your credit history in good standing.

Used strategically, EWA can smooth out your cash flow, reduce financial stress, and help prevent the kinds of missed payments that harm your credit score. In some cases, it can even reduce your reliance on high-cost borrowing options, allowing you to focus on building credit instead of recovering from debt.

In this guide, we’ll break down:

- How earned wage access works

- The different types of EWA programs and how to qualify

- How EWA compares to payday loans and credit card cash advances

- The key benefits and potential drawbacks of EWA

- How pairing EWA with tools like Ava Finance can help you strengthen your credit profile and work toward long-term financial stability

What Is Earned Wage Access (EWA)?

Earned Wage Access (EWA) is a financial service that allows employees to access a portion of their earned but unpaid wages before their scheduled payday. Unlike a traditional loan, this is your own money—you’ve already worked the hours to earn it, so there’s no debt involved in accessing it.

When you use an EWA service, repayment is typically automatic and happens in one of two ways:

- Payroll Deduction – The advanced amount is subtracted from your next paycheck before it’s deposited into your account.

- Bank Account Debit – The provider withdraws the repayment amount directly from your checking account shortly after payday.

EWA services vary by provider, but many:

- Do not require a credit check, meaning using the service won’t result in a hard inquiry on your credit report.

- Allow withdrawals ranging from $35 to $500 per transaction, depending on your earnings and the provider’s rules.

- Offer instant or same-day transfers for an additional fee, making funds available within minutes instead of days.

By giving you faster access to your earnings, EWA can help you:

- Pay bills on time, which is critical for maintaining a positive credit history and avoiding negative marks on your credit report.

- Prevent overdraft fees and late payment charges, both of which can harm your budget and financial stability.

- Manage irregular expenses—such as car repairs, medical bills, or seasonal costs—without relying on payday loans or high-interest credit card cash advances.

When paired with smart money management and credit-building tools like Ava Finance, EWA can also help you indirectly improve your credit score by ensuring bills are paid promptly and consistently. Over time, that reliability can translate into a stronger credit profile, better loan terms, and access to more competitive financial products.

Types of Earned Wage Access Programs

Not all Earned Wage Access programs (EWAPs) are the same. The way you access your funds, the fees you pay, and the speed at which you receive your money can vary depending on the type of program. Understanding these differences is key to choosing an EWA solution that best supports your cash flow management and aligns with your credit-building goals.

Here are the three primary types of EWA programs:

1. Employer-Sponsored EWAPs

Employer-sponsored programs are fully integrated into your company’s payroll system.

- Seamless Access: Because they’re linked directly to payroll, you can quickly withdraw a portion of your earned wages before payday without additional paperwork.

- Direct Deposit Options: Funds are usually sent straight to your bank account or onto a linked payroll debit card.

- Lower Fees: Employer partnerships often mean reduced transaction costs compared to independent providers.

- Credit-Building Advantage: By helping you pay bills on time and avoid late fees, these programs can indirectly protect your credit history and maintain a positive credit report.

2. Third-Party EWAP Providers

These are independent financial technology platforms that partner with employers to provide EWA services.

- Payroll Data Sharing: The provider accesses your time and earnings information through your employer’s payroll system to determine how much you can withdraw.

- Flexible Access: Withdrawals are often available via bank transfer, prepaid debit card, or digital wallet.

- Fee Structure: May include per-transaction fees, monthly subscription fees, or optional “tips” to speed up funding.

- Credit Impact: While they don’t directly report to credit bureaus, timely access to your wages can help you maintain a consistent payment history—key for credit building.

3. Direct-to-Consumer EWAPs

These programs operate independently from employers, making them accessible to workers whose companies don’t offer EWA.

- Direct Deposit Requirement: You’ll usually need to route your paycheck—or a portion of it—into an account with the EWA provider.

- Proof of Income: Many require verification of recurring income or a minimum employment history before granting access.

- Flexibility: Ideal for gig workers, freelancers, and employees at companies without EWA benefits.

- Potential Costs: May charge transaction fees, expedited funding fees, or require a subscription.

- Credit Benefits: While they don’t report activity directly to credit bureaus, they can still support your credit score improvement efforts by ensuring you can pay recurring bills (like utilities, rent, or loan payments) on time—protecting your credit history.

How to Qualify for EWA

While requirements differ by provider, common qualifications include:

- Being employed with a participating employer (for employer-based EWAs).

- Meeting minimum tenure requirements (e.g., 30–90 days).

- Linking an active checking account or debit card.

- Having direct deposit set up for your paychecks.

Direct-to-consumer EWAs may have additional requirements like proof of income or specific account verification.

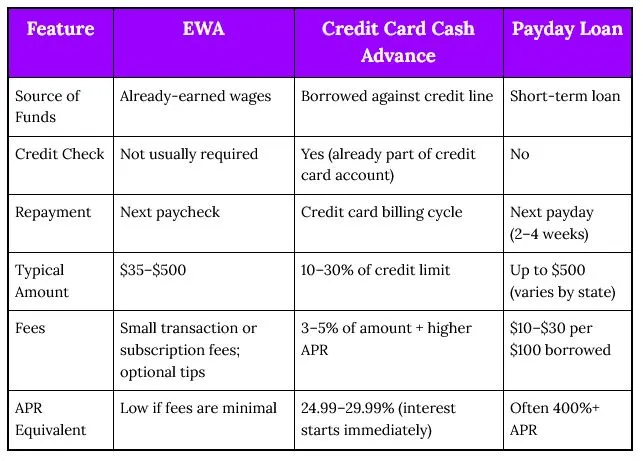

EWA vs. Cash Advances vs. Payday Loans

It’s important to understand how EWA compares to other short-term funding options.

Potential Risks and Considerations

EWA is not without its downsides:

- Overuse Can Hurt Your Next Paycheck: Borrowing too much too often can create a cycle where every payday starts in the negative.

- Fees Add Up: Even small transaction fees can accumulate over time.

- Budget Impact: Without a plan, early withdrawals can make managing your next pay period harder.

Best Practices for Using Earned Wage Access Wisely

- Start Small – Only take what you need, ideally once per pay cycle.

- Budget for the Shortfall – If you withdraw $100 early, cut $100 from expenses next period.

- Track Your Usage – Avoid overlapping withdrawals from multiple EWA platforms.

- Explore Expense Reduction – Negotiate bills, cut discretionary spending, or shift bill due dates.

- Increase Earnings Where Possible – Overtime, side gigs, or skill-based work can close gaps without frequent EWA reliance.

How Earned Wage Access Can Tie Into Credit Building

While most Earned Wage Access (EWA) providers do not report activity directly to the major credit bureaus—meaning EWA itself won’t appear on your credit report—it can still play a valuable role in credit score improvement when used strategically.

The key lies in how you use the funds you access. When paired with strong money management habits and tools like Ava Finance, EWA can help you protect and enhance your credit history, which directly influences your overall credit score.

Here’s how:

1. Supports On-Time Bill Payments

Your payment history accounts for roughly 35% of your FICO® credit score, making it the single most important scoring factor.

- Problem: Late payments can remain on your credit report for up to seven years, significantly hurting your score.

- Solution: By accessing your earned wages early, you can cover critical payments—like credit card bills, rent, or loan installments—before their due dates, keeping your payment history spotless.

2. Helps Avoid Overdrafts and Late Fees

Unexpected shortfalls can force you to miss payments or rely on costly overdraft protection, both of which can strain your budget.

- With EWA: You can prevent these disruptions by using a portion of your wages to bridge the gap until payday, ensuring your accounts stay positive.

- Credit Impact: Avoiding missed payments reduces the risk of negative marks on your credit report, helping maintain your credit score.

3. Reduces Reliance on High-Interest Debt

Without EWA, many people turn to payday loans, credit card cash advances, or other high-APR borrowing to cover urgent expenses. These can quickly lead to debt cycles that make credit building difficult.

- Benefit of EWA: Because you’re using money you’ve already earned, you avoid taking on new debt, which helps keep your credit utilization ratio in check—a factor that accounts for about 30% of your credit score.

4. Leverages Ava Finance for Direct Credit Building

While EWA helps you stay current on bills, Ava Finance takes it further by turning those on-time payments into positive credit history.

- Ava reports eligible recurring payments—such as utilities, streaming subscriptions, and rent—to major credit bureaus.

- This activity adds more positive entries to your credit report, strengthening your profile over time.

Bottom line: EWA can serve as a credit protection tool, ensuring you have the liquidity to pay bills on time and avoid financial pitfalls that harm your credit. When combined with Ava Finance’s reporting features, it transforms from a short-term cash flow solution into a long-term credit-building strategy that can help you achieve higher scores and better loan terms.

Conclusion: How Ava Finance Complements Earned Wage Access

Earned Wage Access (EWA) can be a game-changer for managing short-term cash flow. By giving you the ability to tap into wages you’ve already earned, it helps you cover bills, avoid overdrafts, and reduce reliance on high-interest borrowing options like payday loans or credit card cash advances. This not only eases financial stress but also helps prevent the missed payments that can negatively impact your credit report and slow your credit score improvement.

However, EWA alone doesn’t directly build your credit history—it simply helps you stay current on obligations. To transform short-term liquidity into long-term credit-building success, pairing EWA with Ava Finance is the key.

Ava Finance works by reporting eligible recurring bill payments—such as rent, utilities, and subscriptions—to major credit bureaus, adding positive payment history to your credit report. Over time, this consistent reporting strengthens your credit profile, improves your credit score, and increases your chances of qualifying for better loan terms, higher credit limits, and premium financial products.

By combining the flexibility of EWA with Ava’s credit-building technology, you get the best of both worlds:

- Immediate financial relief when you need to cover expenses before payday.

- Long-term credit growth that unlocks greater financial opportunities.

The bottom line: EWA supports your financial stability today. Ava Finance ensures that stability turns into measurable progress toward a stronger credit score and healthier credit history tomorrow. Together, they create a powerful path toward lasting financial freedom.