If you’ve built equity in your home and want to tap into it for major projects, emergency expenses, debt consolidation, or long-term investments, a Home Equity Line of Credit (HELOC) can be one of the most flexible and cost-effective borrowing options available.

A HELOC lets you borrow against the equity you’ve accumulated—essentially the portion of your home you own outright—often at lower interest rates than unsecured loans or credit cards. This is because a HELOC is a secured loan, using your home as collateral. That security gives lenders confidence to offer more competitive rates, but it also means there’s a serious risk: if you fall behind on payments, you could lose your home.

Beyond the borrowing terms, a HELOC can also impact your credit report, credit history, and credit score. Applying for one involves a hard inquiry that can cause a small, temporary drop in your score. Once open, how you manage your HELOC—such as your repayment habits and the percentage of available credit you use—can either strengthen your credit-building efforts or set them back.

That’s why understanding how a HELOC works, the costs and fees involved, and the potential credit score implications is essential before you apply. In this comprehensive guide, we’ll walk you through:

- How HELOCs operate and what makes them different from home equity loans and personal loans.

- Key features such as draw periods, repayment periods, and interest rate options.

- Common fees and qualification requirements.

- The pros and cons of using a HELOC for various financial needs.

- How to use a HELOC strategically to protect your credit history and even support your credit score improvement goals—especially when combined with tools like Ava Finance.

Used wisely, a HELOC can be more than just a source of funds—it can be part of a bigger strategy to achieve both short-term financial flexibility and long-term credit health.

What Is a HELOC and How Does It Work?

A Home Equity Line of Credit (HELOC) is a revolving line of credit that lets you borrow against the equity you’ve built in your home. Similar to how a credit card works, you can borrow funds up to an approved credit limit, repay what you’ve used, and borrow again—making it a flexible solution for ongoing or unpredictable expenses.

Your credit limit is primarily based on the amount of equity in your property, along with factors like your credit score, income, and debt-to-income ratio.

Understanding Home Equity:

Home equity is the difference between your home’s current market value and the amount you still owe on your mortgage.

- Example: If your home is worth $400,000 and your remaining mortgage balance is $250,000, you have $150,000 in equity.

- Lenders often allow you to borrow up to 85% of your home’s value minus your mortgage balance—though exact limits vary.

Because a HELOC is a secured loan backed by your home, it typically offers lower interest rates than unsecured borrowing options like personal loans or credit cards. This makes it attractive for large projects or debt consolidation. However, this also comes with higher stakes: your home serves as collateral, so falling behind on payments could lead to foreclosure.

How It Works in Practice:

- During the draw period—often 5 to 10 years—you can withdraw funds as needed, up to your limit.

- You may only be required to make interest-only payments during this time, keeping monthly costs lower.

- Once the draw period ends, you enter the repayment period, where you must repay both principal and interest—often over 10 to 20 years.

Impact on Your Credit:

Opening a HELOC typically involves a hard credit inquiry, which can temporarily lower your score by a few points. Once open, how you manage your HELOC—such as making on-time payments and keeping your balance low relative to your limit—can either strengthen your credit history and credit report or harm them if mismanaged. Responsible use can support credit score improvement, especially if you maintain low utilization and never miss a payment.

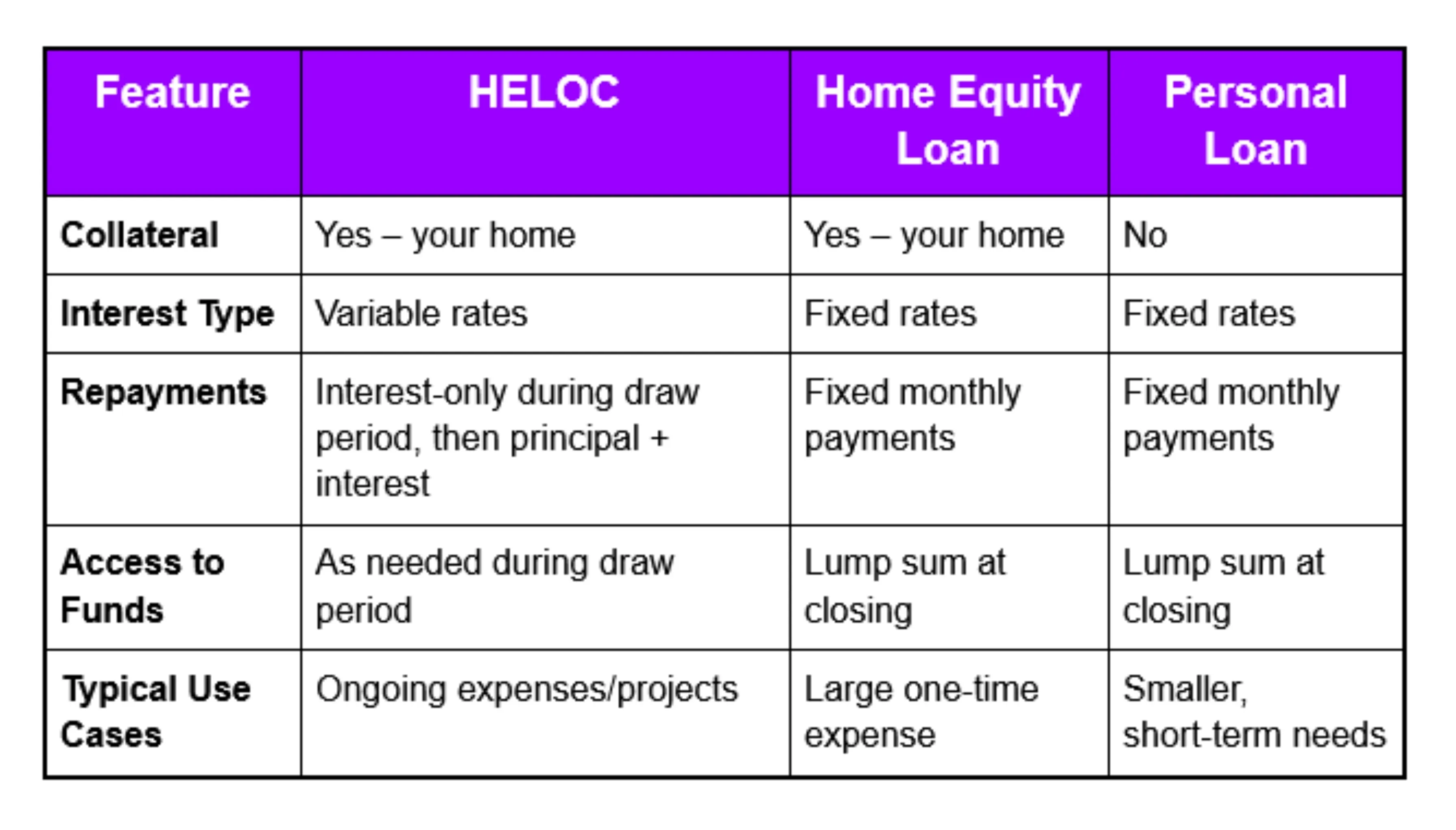

How a HELOC Differs from Other Loans

When considering how to access funds, it’s important to compare HELOCs with home equity loans and personal loans:

Key takeaway: HELOCs provide flexibility—ideal for projects where costs happen over time—while home equity loans are better for fixed expenses. Personal loans are unsecured, have faster approval times, but often come with higher interest rates.

Common Uses for a HELOC

One of the biggest advantages of a Home Equity Line of Credit (HELOC) is its flexibility. Because you can draw funds as needed during the draw period (typically 5 to 10 years), you can match your borrowing to the timing of your expenses—without paying interest on unused funds. This makes HELOCs especially useful for a variety of situations:

1. Home Improvements & Renovations

HELOCs are a popular choice for multi-phase renovations or ongoing home upgrades because you can access funds in stages as work progresses.

- Examples include kitchen remodels, bathroom upgrades, adding an outdoor living space, or making energy-efficient improvements like solar panels or upgraded insulation.

- Not only can these projects improve your quality of life, but they may also increase your home’s market value, potentially boosting your home equity over time.

- Because HELOC rates are typically lower than personal loans or credit cards, you could save significantly on financing costs for large-scale home projects.

2. Debt Consolidation

If you’re carrying high-interest debt—such as credit card balances or personal loans—a HELOC can be an effective tool for debt consolidation.

- By paying off these debts with a lower-interest HELOC, you can reduce monthly payments and save money on interest over the long term.

- Strategically, this can also help improve your credit utilization ratio, which is a key factor in your credit score.

- However, it’s essential to commit to responsible spending after consolidation; otherwise, you risk running up new debt while still owing on the HELOC.

3. Emergency Expenses

Life is unpredictable, and having access to funds during emergencies can be a financial lifesaver.

- HELOCs can cover unexpected medical bills, major car repairs, or urgent travel needs without having to rely on costly payday loans or credit card cash advances.

- Using a HELOC instead of maxing out credit cards can help protect your credit report from negative utilization spikes and keep your credit history in good standing.

4. Education or Career Development (Optional but Common Use)

Some homeowners use HELOC funds for tuition, certifications, or career training—expenses that may increase future earning potential.

- While not a primary recommendation for all borrowers, investing in your skills and career can be a strategic long-term move, especially if the HELOC rate is lower than private student loan rates.

Bottom line: Whether you use it for home upgrades, debt reduction, or unexpected costs, a HELOC offers flexible access to funds at competitive rates. Just remember—because your home is the collateral, it’s crucial to borrow strategically and make consistent, on-time payments to protect both your property and your credit score.

Key HELOC Terms to Understand

When considering a Home Equity Line of Credit (HELOC), it’s essential to understand the two main phases that determine how and when you can access funds, as well as how your repayment structure will work. These phases can significantly affect your monthly budget, your credit history, and even your credit score if managed incorrectly.

1. Draw Period

The draw period is the initial phase of your HELOC, typically lasting 5 to 10 years. During this time, you can borrow funds up to your approved credit limit, repay them, and borrow again—similar to how a credit card works, but at generally lower interest rates.

Key features of the draw period:

- Interest-Only Payments: Many HELOCs allow you to make interest-only payments during the draw period, which keeps monthly costs lower. However, this also means your principal balance doesn’t decrease unless you make extra payments.

- Flexible Borrowing: Funds can be withdrawn as needed for home renovations, debt consolidation, or emergency expenses, making it ideal for ongoing or phased projects.

- Impact on Credit Utilization: Using too much of your available HELOC limit can raise your credit utilization ratio—a factor that can influence your credit score—so it’s wise to keep usage balanced.

2. Repayment Period

Once the draw period ends, you enter the repayment period, which typically lasts 10 to 20 years. At this stage, you can no longer withdraw funds from your HELOC, and your payment structure changes significantly.

Key features of the repayment period:

- Principal + Interest Payments: Payments will now include both the original borrowed amount (principal) and interest, which can cause your monthly payment to increase substantially compared to the draw period.

- Budget Adjustment: This shift often requires a budget review to ensure you can comfortably handle the higher payments without missing due dates—missed or late payments can negatively impact your credit report and credit history.

- Payoff Strategies: Paying more than the minimum due or making lump-sum payments when possible can help reduce interest costs and improve your overall debt-to-income ratio.

Why This Matters for Your Credit

Understanding the difference between the draw and repayment phases is critical for managing your HELOC responsibly. By making on-time payments throughout both periods, you protect your payment history, which is the single largest factor in your credit score. Consistent repayment also strengthens your credit profile, making you more attractive to lenders for future borrowing opportunities.

Fixed vs. Variable Interest Rates on a HELOC

One of the most important factors to understand when taking out a Home Equity Line of Credit (HELOC) is how your interest rate works. Interest rates directly influence your monthly payments, the total cost of borrowing, and—if not managed carefully—your ability to maintain a strong credit history and healthy credit score.

Variable Interest Rates

Most HELOCs start with variable interest rates, which means the rate can rise or fall over time based on a financial benchmark, such as the U.S. prime rate or another market index.

Key points about variable rates:

- Lower Initial Rates: Variable rates often start lower than fixed rates, making them appealing for borrowers who want a lower initial monthly payment.

- Monthly Payment Fluctuations: If market interest rates rise, your monthly payments will increase, which could strain your budget and make it harder to pay on time. Missed or late payments can negatively impact your credit report.

- Potential for Savings: If interest rates drop, your payments may decrease, saving you money—but rate changes are unpredictable.

Example:

If your HELOC has an interest rate of 7% tied to the prime rate, and the prime rate increases by 1%, your new rate would be 8%, and your payment amount would increase accordingly.

Fixed Interest Rates

Some lenders offer the option to lock in a fixed rate for part—or sometimes all—of your outstanding HELOC balance. This creates a more predictable repayment schedule.

Key points about fixed rates:

- Predictable Payments: Your rate and payment amount stay the same for the fixed portion, making it easier to budget and avoid missed payments.

- Higher Than Initial Variable Rates: Fixed rates are generally higher than the starting variable rate, so while you gain stability, you may pay more interest in the short term.

- Partial Lock Option: Many lenders allow you to fix the rate on just a portion of your balance, giving you flexibility while managing interest risk.

Example:

If you borrow $50,000 through your HELOC, you might choose to lock $20,000 at a fixed 8% interest rate while keeping the remaining $30,000 at a variable rate—balancing predictability and potential savings.

Which Should You Choose?

- Go Variable if you expect to repay your balance quickly and want to start with lower payments.

- Go Fixed if you want stability in your budget, plan to carry the balance long-term, or expect interest rates to rise.

- Mix Both for a customized strategy that offers security without sacrificing flexibility.

Credit Impact Tip:

Whether you choose fixed or variable, the most important factor for your credit report and credit score is consistent, on-time payments. Payment history makes up 35% of your credit score, so even if rates rise, prioritizing timely payments is essential to protect your financial standing.

HELOC Qualification Requirements

While requirements vary by lender, most will expect:

- 15%–20% home equity

- Credit score of 620 or higher

- Good credit history (on-time payments, no major delinquencies)

- Debt-to-income (DTI) ratio below 43%

- Steady employment and verifiable income

Because your credit score and credit report play a role in approval and interest rate determination, maintaining strong credit habits before applying can improve your borrowing terms.

Costs Associated with a HELOC

Potential fees include:

- Application and origination fees

- Appraisal, title, or closing costs

- Annual or membership fees

- Inactivity fees for unused credit lines

- Early closure fees if you cancel within the first few years

- Conversion fees if switching to a fixed rate

Always compare multiple lenders to find the most competitive combination of interest rate and fees.

Pros and Cons of Using a HELOC

Pros:

- Lower interest rates than unsecured loans or credit cards

- Flexible access to funds during draw period

- Interest-only payments during draw phase

Cons:

- Variable rates can cause payments to rise

- Your home is at risk if you can’t repay

- Fees can add to borrowing costs

- Lender may reduce or freeze your limit if your home value drops

How a HELOC Can Impact Your Credit

A HELOC can affect your credit score and credit report in several ways:

- Hard Inquiry: Applying triggers a hard pull, which may cause a small, temporary dip in your score.

- Credit Utilization: A HELOC is often treated as a revolving account, so high usage can increase your utilization ratio, potentially lowering your score.

- Payment History: Consistently paying on time can strengthen your credit history—missed payments will hurt your score and remain on your credit report for years.

- Account Age: Opening a HELOC can lower your average account age, which may have a small impact on your score initially.

Best Practices for Managing a HELOC

- Borrow only what you need to avoid excessive debt.

- Make more than the minimum payment to reduce principal faster.

- Track interest rate changes if you have a variable rate.

- Budget for the repayment period when payments may rise significantly.

- Pair your HELOC usage with credit-building strategies to maintain or improve your credit score.

Conclusion: Using a HELOC Wisely With Ava Finance

A Home Equity Line of Credit can be a powerful tool for funding large projects, consolidating debt, or handling unexpected expenses—often at lower interest rates than other forms of credit. But because it’s secured by your home, it’s essential to borrow responsibly, make all payments on time, and stay mindful of how it affects your credit history and credit score.

For borrowers who want to take their financial strategy further, Ava Finance can help. While a HELOC can provide access to funds, Ava transforms your regular bill payments into credit-building opportunities, reporting them to major credit bureaus to strengthen your credit report over time. Together, a well-managed HELOC and Ava Finance can give you both short-term flexibility and long-term financial growth—helping you qualify for better rates, higher limits, and more opportunities in the future.