If you’ve noticed your grocery bill creeping higher, your rent renewal costing more than expected, or your favorite streaming service quietly bumping up its monthly price, you’re not imagining things. Inflation continues to squeeze household budgets—making every dollar feel like it doesn’t stretch as far as it once did. While the pace of inflation in 2025 has slowed compared to its peak just a few years ago, the financial pressure remains very real.

The truth is, inflation isn’t just an abstract economic number tossed around in the news. It directly impacts your purchasing power, your savings, your debt load, and even your credit report. The good news? You’re not powerless against it. With smart planning and practical strategies, you can counteract the impact of inflation and keep your finances on track.

In this comprehensive guide, we’ll break down:

- What inflation is and how it affects your everyday money.

- The ripple effects on credit, borrowing, and saving.

- Six powerful strategies to beat inflation at its own game.

- Why building and protecting your credit score is more important than ever.

- How tools like Ava Finance, a credit builder app, can help you future-proof your financial health.

Let’s dive in.

What Exactly Is Inflation and Why Should You Care?

Inflation is often described as the “silent thief” of wealth. At its core, it’s the rate at which the prices of goods and services increase over time. The higher inflation climbs, the less your money can buy—shrinking your purchasing power. Economists measure this change through the Consumer Price Index (CPI), which tracks the prices of everyday necessities like groceries, housing, transportation, and medical care.

Take a recent example:

- In July 2025, the CPI rose 2.7% over the past year, slightly lower than the 2.9% increase recorded the year before.

- Food prices alone jumped 3.1%, with groceries up 2.4% and dining out a steeper 4.1%.

- Housing costs climbed 3.7%, while transportation services rose 3.4%.

At first glance, these numbers may not seem alarming. But inflation’s real danger lies in its compounding effect. A steady 3% annual increase means your $100 grocery bill becomes $103 next year. After five years, the same cart of groceries could cost $116—even if your paycheck hasn’t grown. That slow erosion of purchasing power is what makes inflation a concern for every household.

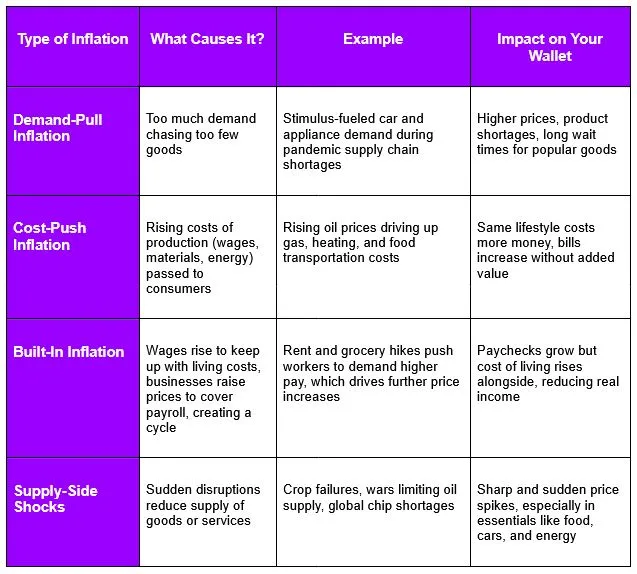

Types of Inflation You Should Know

Not all inflation is created equal. The reason prices rise can tell you a lot about where the economy is headed and how your budget will be affected. Here are the four main types:

How Inflation Affects Your Money and Credit

Inflation doesn’t just raise prices at the store. It affects nearly every corner of your financial life.

- Purchasing Power Shrinks

- Essentials like food, rent, and fuel eat up a larger share of your paycheck.

- Discretionary spending (travel, dining, hobbies) gets cut back, reducing quality of life.

- Borrowing Becomes More Expensive

- To curb inflation, central banks often raise interest rates.

- This trickles down into higher credit card APRs, personal loan costs, and mortgage rates.

- Debt Gets Harder to Manage

- Credit card balances become more expensive to carry if rates climb.

- Missed or late payments due to higher costs can damage your credit report.

- Savings Lose Value

- A $10,000 savings account at a 0.5% interest rate loses purchasing power if inflation is 3–4%.

- Without adjusting where your money is stored, your “safety net” shrinks in real terms.

- Credit Reports Reflect Struggles

- Late payments show up on your credit history.

- High credit utilization (using too much of your available credit) drags your score down.

In short, inflation doesn’t just challenge your budget—it also threatens your long-term financial stability and your credit score.

Six Proven Strategies to Counteract Inflation

Now that we’ve outlined the risks, let’s focus on solutions. These six strategies combine practical budgeting, debt management, savings tactics, and credit-building habits to help you fight inflation without losing financial ground.

1. Track and Rework Your Budget

Inflation makes your old budget outdated. What worked a year ago may no longer cover today’s reality.

Steps to Inflation-Proof Your Budget:

- Audit all expenses: Use apps or spreadsheets to track where your money really goes.

- Cut “silent drains”: Subscriptions, unused memberships, or autopay charges you’ve forgotten about.

- Prioritize essentials: Shelter, food, utilities, and debt payments come first.

- Adopt the 50/30/20 rule (with adjustments): 50% needs, 30% wants, 20% savings—but tweak for rising costs by reducing “wants.”

👉 Example: If inflation pushes your grocery bill up by $100 per month, you might cut $50 from dining out and $50 from streaming/entertainment.

Budgeting isn’t about deprivation—it’s about regaining control and visibility.

2. Identify Inflation Hot Spots in Your Spending

Not all expenses rise equally. Inflation hits some categories harder than others.

High-Inflation Categories and Solutions:

- Food: Buy in bulk, switch to store brands, and meal plan to reduce waste.

- Housing: Consider refinancing, negotiating rent, or moving to lower-cost areas.

- Transportation: Carpool, use public transit, or explore fuel-efficient vehicles.

- Healthcare: Use telehealth, compare pharmacies, and review insurance options.

👉 Fresh Example: If gas prices rise 20%, commuting costs skyrocket. A carpool or remote work option could save you $150+ monthly.

By pinpointing hot spots, you fight inflation with surgical precision rather than across-the-board cuts.

3. Protect Savings with Inflation-Resistant Accounts

Leaving your emergency fund in a low-yield account is like letting inflation steal from you silently.

Better Options:

- High-Yield Savings Accounts (HYSA): Offer 4–5% interest vs. traditional banks’ 0.01%.

- Money Market Accounts (MMA): Higher rates with check-writing access.

- Certificates of Deposit (CDs): Lock in fixed rates for 6–24 months.

- Treasury Inflation-Protected Securities (TIPS): Government bonds that adjust with inflation.

👉 Example: $10,000 in a HYSA at 4.5% grows by $450 in a year. In a traditional account at 0.1%, it earns just $10—a $440 difference.

Security matters too: Always check for FDIC or NCUA insurance to guarantee protection up to $250,000.

4. Prioritize Paying Down High-Interest Debt

Inflation + high-interest debt is a dangerous combo. As prices rise, interest charges eat more of your paycheck.

Focus on:

- Credit cards: APRs often 20%+, and many are variable.

- Personal loans: Rates can climb quickly with inflation.

Strategies:

- Avalanche method: Pay off highest-interest debt first to save money long term.

- Snowball method: Pay off smallest balances first for motivation.

- Balance transfer cards: 0% APR offers (if your credit qualifies).

👉 Example: A $5,000 credit card at 22% APR costs $1,100 annually in interest if unpaid. Paying it down aggressively saves thousands over time.

Eliminating high-interest debt is like giving yourself an instant raise during inflation.

5. Build a Larger Emergency Fund

Rising costs mean your old emergency fund target may no longer cut it.

Updated Guidelines:

- Traditional: 3–6 months of expenses.

- Inflation-adjusted: Aim for 6–9 months, especially if you support dependents.

Tips:

- Automate small transfers weekly instead of large monthly ones.

- Use windfalls (tax refunds, bonuses) to boost savings.

- Keep it liquid (accessible) but earning interest.

👉 Example: If your monthly expenses rise from $3,000 to $3,300 due to inflation, your six-month emergency fund goal jumps from $18,000 to $19,800. Adjust accordingly.

An emergency fund is your buffer against inflation shocks, job loss, or unexpected bills.

6. Invest to Outpace Inflation

Savings accounts protect money, but they may not grow fast enough to beat long-term inflation. That’s where investing comes in.

Options:

- Stocks/ETFs: Historically average 7–10% annual returns.

- Bonds: Lower returns but more stability.

- REITs (Real Estate Investment Trusts): Inflation hedge through property income.

- Index Funds: Broad exposure with low fees.

Risk Management:

- Diversify across asset classes.

- Adjust allocations based on your risk tolerance.

- Avoid panic-selling during volatility.

👉 Example: $10,000 invested in the S&P 500 has historically grown to over $40,000 in 20 years—despite periods of high inflation.

Investing isn’t about quick wins—it’s about long-term protection and growth.

The Psychological Side of Inflation

Inflation doesn’t just hurt your wallet—it messes with your mindset.

- Anxiety: Rising bills create uncertainty.

- Scarcity mentality: Leads to panic saving or overspending.

- Decision fatigue: Constantly adjusting makes money feel overwhelming.

How to Stay Resilient:

- Focus on what you can control (budgeting, debt, saving).

- Practice mindfulness to reduce money stress.

- Remember: Inflation is cyclical—it will eventually ease.

Financial health is as much about emotional balance as dollars and cents.

Credit and Inflation: The Overlooked Link

Here’s what many miss: inflation can indirectly damage your credit report and score.

- Late payments: Rising costs = more missed bills.

- High credit utilization: Using cards to cover expenses raises your utilization ratio, a key credit factor.

- Limited borrowing options: Poor credit makes inflationary periods harder to navigate.

Why Building Credit Is Essential

- A strong credit score lowers borrowing costs.

- Better terms on mortgages, auto loans, and credit cards save thousands.

- Employers and landlords may review credit reports for trustworthiness.

This is where Ava Finance makes a difference.

How Ava Finance Helps:

- Reports rent, utilities, and phone payments to all three credit bureaus.

- Builds credit without requiring a credit card or loan.

- Gives you a simple, low-risk way to add positive history to your credit report.

👉 With inflation increasing financial strain, building credit with bills you already pay is one of the smartest moves you can make.

Frequently Asked Questions

Q: What causes inflation?

A: Inflation can be demand-driven (too much spending), cost-driven (higher production costs), or caused by supply shocks (like oil shortages).

Q: How much should I keep in an emergency fund during inflation?

A: At least 6–9 months of essential expenses, adjusted for higher prices.

Q: Is investing risky during inflation?

A: All investing carries risk, but diversified, long-term investing often outpaces inflation over decades.

Q: Can inflation ever help with debt?

A: Yes—if you hold fixed-rate loans (like a mortgage), inflation reduces the “real value” of your payments over time. But variable-rate debt becomes more expensive.

Conclusion: Take Control of Your Money with Ava Finance

Inflation may feel like an unstoppable force, but your response determines its impact on your life. By reworking your budget, focusing on inflation-prone expenses, protecting savings, paying down debt, building a stronger emergency fund, and investing smartly, you can shield your finances and even come out stronger.

But don’t overlook your credit health. A strong credit score reduces borrowing costs, improves access to financial opportunities, and provides resilience when prices rise.

That’s where Ava Finance comes in. By reporting everyday bills like rent and utilities to all three major credit bureaus, Ava helps you build credit without new loans, credit cards, or risky products. In today’s inflationary world, that’s a game-changer.

👉 Don’t let inflation hold you back. Take control of your financial future with Ava Finance today.