Picture this: You’re finally ready to take charge of your financial future, but when it comes to choosing a credit card, you’re hit with two options — secured and unsecured credit cards. One requires a deposit, the other doesn’t. One feels more accessible, the other offers rewards and higher limits. Which one should you choose to build or rebuild your credit score?

This decision can significantly impact your financial journey. The right credit card can help you establish a strong credit history, improve your credit score, and open doors to better loans, lower interest rates, and financial freedom. The wrong choice could set you back with unnecessary fees, high interest, or even debt struggles.

This guide breaks down everything you need to know about secured and unsecured credit cards — how they work, how they affect your credit report, and which option is right for your situation.

What’s in this Article?

- What is a Secured Credit Card?

- Pros and Cons of Secured Credit Cards

- What is an Unsecured Credit Card?

- Pros and Cons of Unsecured Credit Cards

- Key Differences Between Secured and Unsecured Cards

- How to Apply for Each Type of Card

- Do You Get Your Security Deposit Back?

- How Credit Cards Help Build Credit

- On-Time Payments

- Credit Utilization

- Paying Balances in Full

- Monitoring Your Credit Report

- Which Credit Card Type Is Better for You?

- Building Credit Beyond Credit Cards with Ava Finance

What is a Secured Credit Card?

A secured credit card works much like a traditional unsecured credit card, with one key difference: you must provide a security deposit upfront before you can use it. This deposit acts as collateral for the lender, giving them financial protection if you fail to make payments.

For example:

- If you put down a $500 deposit, your credit limit will usually be set at $500.

- Some issuers allow you to deposit more (say $1,000), which raises your credit limit accordingly.

- After demonstrating several months of responsible use — making on-time payments and keeping balances low — many card issuers will either increase your credit limit without requiring more money or even “graduate” you to an unsecured credit card with better terms.

This makes secured credit cards especially attractive for people who are trying to:

- Rebuild credit after financial hardship (such as collections, charge-offs, or bankruptcy).

- Establish credit for the first time (students, young adults, or recent immigrants with no U.S. credit history).

- Improve a weak credit score in order to qualify for loans or better interest rates in the future.

Because the security deposit reduces the bank’s risk, approval is usually much easier than with an unsecured card. In fact, some issuers don’t even perform a hard credit check for secured card applications, making them accessible even for those with bad credit.

Important Distinction: Secured Credit Cards vs. Prepaid Debit Cards

Many people confuse secured credit cards with prepaid debit cards, but they are not the same. Here’s the difference:

- Prepaid debit cards: You load money onto the card and spend it down. Once the money is gone, you must reload the card. They don’t involve borrowing money from a lender, so they don’t appear on your credit report and have no impact on your credit score.

- Secured credit cards: Even though you’ve provided a deposit, you’re still borrowing money from the issuer each time you make a purchase. You must repay those charges monthly, just like with an unsecured card. Your payment activity is reported to all three major credit bureaus — Experian, Equifax, and TransUnion. This reporting is what allows secured cards to actively build or rebuild your credit history.

Key Takeaway: A secured credit card is essentially a tool to prove your creditworthiness when you don’t yet qualify for unsecured options. Used correctly — paying on time, keeping balances low, and avoiding interest charges — it can become one of the fastest, safest ways to improve your credit report and raise your credit score.

Pros and Cons of Secured Credit Cards

Like any financial tool, secured credit cards come with both advantages and disadvantages. Understanding these can help you decide whether this type of card fits your financial goals and credit-building strategy.

Pros of Secured Credit Cards

- Great for Building or Rebuilding Credit

Secured credit cards are designed for people with little to no credit history or those recovering from past credit mistakes such as late payments, charge-offs, or bankruptcy. Since most secured cards report your payment activity to all three major credit bureaus — Experian, Equifax, and TransUnion — they can directly impact your credit report and improve your credit score over time. - Encourages Responsible Habits

Because you’ve put down a cash deposit to open the account, you have a financial incentive to use the card wisely. Making consistent, on-time payments protects your deposit and helps you avoid losing money, which naturally motivates better money management. - Easier Approval

Unlike unsecured credit cards that require a good or excellent credit score, secured cards are much easier to get approved for. Since the deposit reduces risk for the lender, applicants with bad credit or even no credit history often qualify. - No Major Credit Requirement

Some issuers don’t perform a hard credit inquiry, which means applying for a secured card won’t hurt your credit score. This makes them an accessible option if you’re just starting out or want to avoid unnecessary inquiries on your credit report.

Cons of Secured Credit Cards

- Security Deposit Required

The biggest drawback is the upfront cash requirement. Most secured cards require a deposit ranging from $200 to $500 or more. For someone rebuilding finances, tying up that money may be a burden — especially since you can’t use it to pay your monthly bill. - Fees Can Add Up

Secured cards often come with fees that eat into their value. These may include annual fees, application fees, or late payment fees. Some cards even charge monthly maintenance fees, so it’s important to read the fine print. - Higher APRs

Many secured credit cards carry high interest rates (APRs) — often 20% or more. If you carry a balance from month to month, you could quickly rack up interest charges. This makes paying your balance in full every month especially important. - Low Credit Limits

Credit limits on secured cards are usually equal to your deposit, which means your spending power may be limited. For example, a $300 deposit gives you a $300 credit limit. This makes it harder to keep your credit utilization ratio low, which is an important factor in your credit score. (Ideally, you should use less than 30% of your available credit.)

Bottom Line: Secured credit cards are powerful tools for credit building, but they work best when you can afford the deposit, manage fees, and pay your balance in full every month.

What is an Unsecured Credit Card?

An unsecured credit card is the most common type of credit card used today. Unlike a secured credit card, it doesn’t require a security deposit to open. Instead, the credit card issuer relies on your creditworthiness — things like your credit score, income level, payment history, and debt-to-income ratio — to decide whether to approve you.

For example:

- If you have excellent credit (a score above 720), you might be approved for a $2,000 or higher credit limit with a lower APR and attractive perks like cashback rewards.

- If your credit score is average or fair (580–669), you may still qualify, but your limit may be much lower, and your APR could be significantly higher.

Because there’s no deposit involved, unsecured cards are riskier for lenders, so approval standards are stricter. Still, for those who qualify, they can offer powerful benefits such as cashback, airline miles, hotel rewards, and purchase protections.

Pros and Cons of Unsecured Credit Cards

Pros of Unsecured Credit Cards

- No Upfront Deposit Required

Unlike secured cards, you don’t need to come up with $200–$500 (or more) to secure the account. This makes them accessible to people who have decent credit but don’t want to tie up cash in a deposit. - Rewards and Perks

Unsecured credit cards often come with a wide range of benefits that secured cards rarely offer:

- Cashback programs: Get 1–5% back on purchases, either as statement credits or cash rewards.

- Travel points & miles: Earn rewards redeemable for flights, hotels, or vacation packages.

- Sign-up bonuses: Many cards offer introductory bonuses like “Earn $200 after spending $1,000 in the first 3 months.”

- Additional perks: Some premium cards include airport lounge access, extended warranties, or rental car insurance coverage.

These perks can translate into significant savings if you use your card strategically.

- Higher Credit Limits

Approval for an unsecured card is based on your creditworthiness, which means you may qualify for much higher credit limits than you would on a secured card. Higher limits can make it easier to keep your credit utilization ratio (the percentage of credit used vs. available) below the recommended 30%, which directly benefits your credit score.

Cons of Unsecured Credit Cards

- Harder to Qualify For

Because lenders take on more risk without a deposit, unsecured cards generally require at least fair to good credit to be approved. If your credit report shows negative items like late payments, charge-offs, or collections, you may face denials or only qualify for unsecured cards with less attractive terms (high APRs, low limits, or annual fees). - Risk of Overspending

A higher credit limit gives you more financial flexibility, but it also comes with the temptation to overspend. Without discipline, it’s easy to rack up balances that are difficult to pay off, leading to debt cycles that can hurt your credit score and long-term financial health. - Possible High APRs

Even if you’re approved, your APR (Annual Percentage Rate) depends on your credit profile. Someone with excellent credit might enjoy a 15% APR, while someone with average credit may face rates closer to 25%–30%. Carrying a balance on a high-interest unsecured card can quickly become expensive.

Bottom Line: Unsecured credit cards can be powerful tools for those with established credit history, offering higher limits and valuable rewards. However, they require more responsibility and stronger credit scores to unlock their full potential. If you don’t yet qualify for one, starting with a secured card — or using a credit builder tool like Ava Finance — may be the smarter path.

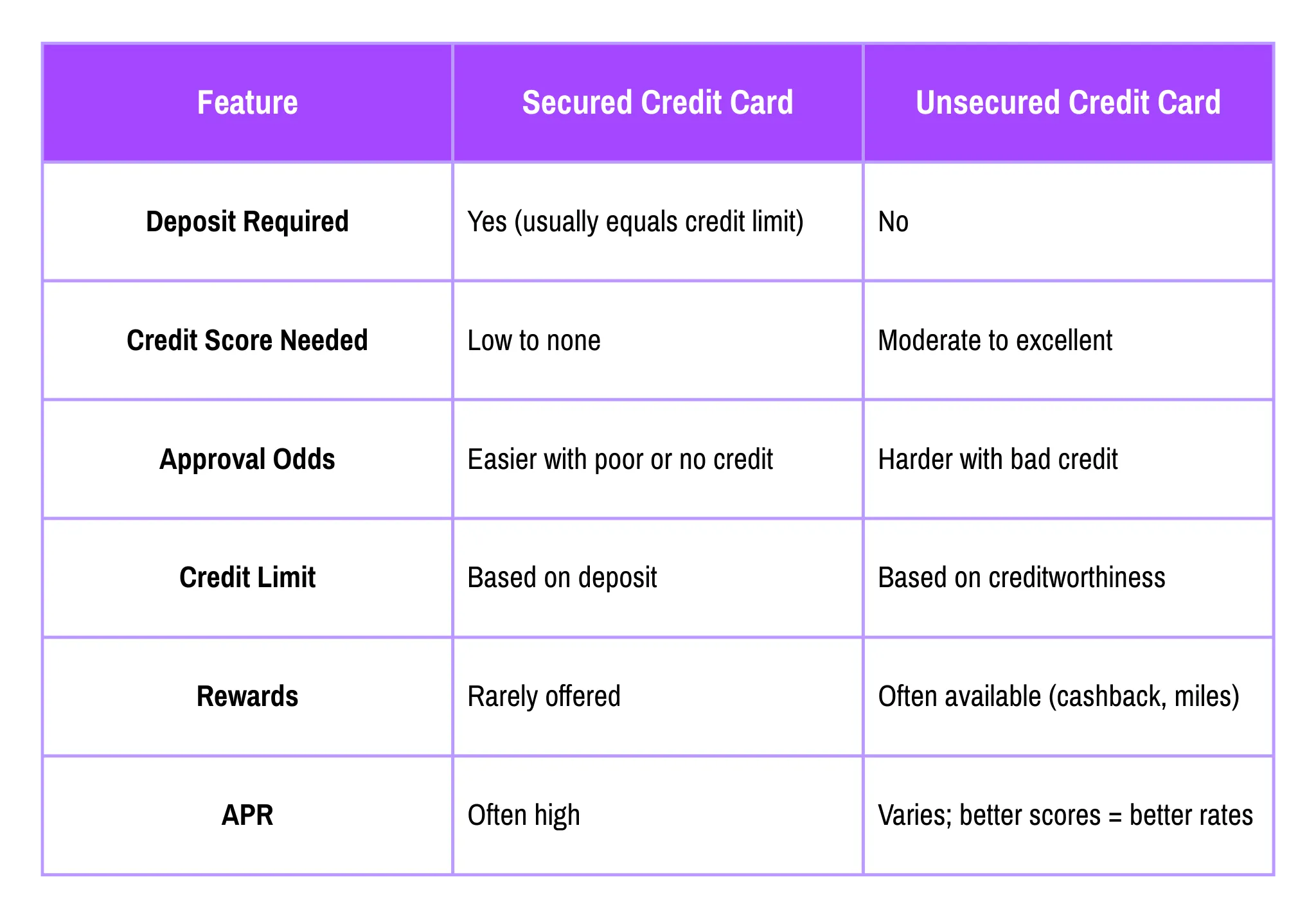

Key Differences Between Secured and Unsecured Cards

While both card types help build credit when used responsibly, here are the core differences:

In short: Secured cards are training wheels — reliable for building a foundation. Unsecured cards are the upgrade, offering perks once your credit history improves.

How to Apply for a Secured Credit Card

The process of applying for a secured credit card is usually simpler than applying for an unsecured one because lenders already have the reassurance of your security deposit. Still, there are a few steps and requirements to be aware of:

1. Provide Proof of Identity

Like any credit card application, you’ll need to verify your identity. This typically means providing:

- Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN)

- Date of birth

- Current address and sometimes proof of residence (like a utility bill)

- Contact details

This step ensures that the credit card issuer can accurately report your activity to the major credit bureaus — Experian, Equifax, and TransUnion — which is how secured cards help you build or rebuild your credit report.

2. Deposit Funds (Security Deposit)

The defining feature of a secured card is the required refundable security deposit. Most issuers ask for a minimum deposit of $200–$500, though some allow deposits up to several thousand dollars.

- Example: A $500 deposit typically gives you a $500 credit limit.

- Some issuers let you add more to your deposit later if you want to increase your limit.

- Your deposit remains with the bank and is only used if you default on your payments.

Because your credit limit is tied to your deposit, it’s important to think strategically about how much you can afford to set aside. The more you deposit, the more room you have to manage your credit utilization ratio, which makes up 30% of your credit score.

3. Avoid Recent Bankruptcies or Severe Credit Issues

While secured cards are far easier to qualify for than unsecured ones, approval isn’t automatic. Some issuers may deny applications if your credit report shows very recent bankruptcies, foreclosures, or ongoing delinquencies.

That said, many secured cards are designed specifically for consumers with poor or no credit history. As long as you meet the deposit and identity requirements, your chances of approval are typically much higher than with traditional cards.

4. Graduating to an Unsecured Card

One of the biggest benefits of secured credit cards is that they can serve as a stepping stone to an unsecured card. Many issuers review your account after 6–12 months of on-time payments. If you’ve managed the card responsibly, they may:

- Upgrade you to an unsecured card with a higher limit and better perks.

- Refund your deposit while allowing you to keep the account open (helping your credit age).

- Offer you access to other financial products, such as loans, at more favorable terms.

This transition can be a huge milestone in your credit building journey — proving to lenders that you’re now a lower-risk borrower.

Key Takeaway: Applying for a secured credit card is a straightforward process, but its real value comes from how you use it. By making on-time payments, keeping your balances low, and monitoring your credit report, you can leverage a secured card as your gateway to better credit opportunities in the future.

Do You Get Your Deposit Back?

Yes — in most cases, the deposit you provide for a secured credit card is fully refundable. Think of it as collateral rather than a fee. Here’s how it usually works:

- If you close the account in good standing: As long as your balance is paid in full and you don’t owe any fees, the issuer will return your deposit when you close the account. For example, if you put down a $500 deposit and later close the account with a zero balance, you’ll receive your $500 back.

- If your account graduates to an unsecured card: Many secured card issuers review your account after 6–12 months of responsible use. If you’ve consistently made on-time payments and managed your balance well, they may “upgrade” you to an unsecured credit card. In that case, your security deposit will be refunded, and you’ll continue using your account as a regular credit card.

- If you default on payments: The deposit is meant to protect the lender, so if you fall behind or fail to pay your balance, the issuer may use your deposit to cover what you owe. Even then, if your debt exceeds the deposit amount, you could still owe additional money.

Key Takeaway: Your deposit isn’t a cost, it’s a safeguard. Treat your secured card like any other credit card — make on-time payments, keep balances low, and use it strategically to build your credit score. That way, you’ll eventually get your deposit back and strengthen your credit report in the process.

How to Apply for an Unsecured Credit Card

Applying for an unsecured credit card is typically quick and convenient, since most applications are available online and decisions can often be made within minutes. However, because these cards don’t require a deposit, approval depends heavily on your creditworthiness.

Here are the steps to improve your approval odds:

1. Check Your Credit Score First

Your credit score plays the biggest role in determining which cards you may qualify for.

- Excellent Credit (720+) → Access to premium cards with the best rewards, perks, and lowest APRs.

- Good Credit (670–719) → Approval for many mid-tier rewards cards with reasonable rates.

- Fair Credit (580–669) → Limited options, often starter unsecured cards with modest limits.

- Poor Credit (<580) → Very few unsecured cards available; may need to start with a secured card or credit builder loan instead.

2. Apply for Cards Suited to Your Score Range

Avoid wasting applications on cards out of your reach. Every application creates a hard inquiry on your credit report, which can temporarily lower your score by a few points. Applying for multiple cards you don’t qualify for can make things worse.

Example: If your score is 640, applying for a premium travel rewards card requiring 700+ is likely a wasted attempt. Instead, look for cards marketed as “fair credit” or “rebuilding credit” to increase your approval chances.

3. Prepare Your Information

When applying, most issuers will ask for:

- Personal details (name, SSN/ITIN, address, and date of birth).

- Income and employment information to gauge your ability to repay.

- Housing costs (rent or mortgage payments) to assess your debt-to-income ratio.

Make sure all information matches your credit report to avoid delays or rejections.

4. Expect a Hard Inquiry

Nearly all unsecured card applications involve a hard credit check, which temporarily lowers your score by 2–5 points. This is normal, and the effect usually fades within a few months as long as you keep managing your credit responsibly.

5. Compare Offers Beyond Approval Odds

Even if you qualify, not all unsecured cards are created equal. Compare:

- APR (Annual Percentage Rate) – lower is better if you may carry a balance.

- Fees – some cards charge annual or foreign transaction fees, while others don’t.

- Rewards – consider cashback, points, or travel perks based on your lifestyle.

- Introductory Offers – look for 0% APR promotions or sign-up bonuses if available.

Key Takeaway: Applying for an unsecured card is easy, but approval depends on your credit score and credit report. Always apply strategically — for cards that fit your current credit profile — to maximize your chances of getting approved and avoid unnecessary hard inquiries.

How Credit Cards Help Build Credit

Regardless of type, both secured and unsecured cards can improve your credit report and credit score when used wisely.

1. Make On-Time Payments

Payment history makes up 35% of your credit score. Even one late payment can hurt. With secured cards, missing payments could also cost your deposit.

2. Keep Credit Utilization Low

Credit utilization — how much of your available credit you use — makes up about 30% of your score. Keep balances below 30% of your limit.

- Example: With a $300 secured card, don’t spend more than $90 without paying it down.

3. Pay Balances in Full

Carrying a balance racks up interest and raises utilization. Paying in full every month is the smartest way to build credit.

4. Monitor Your Credit Reports

Always review your credit report for accuracy. You can get free weekly reports at annualcreditreport.com. Watch for errors, duplicate accounts, or inaccurate late payments.

Which Credit Card Type Is Better for You?

The “best” credit card depends on your financial situation and goals:

- Choose a secured credit card if:

- You’re just starting out with no credit history.You’ve had past credit challenges (late payments, charge-offs, collections).

- You want a safe way to rebuild and prove financial responsibility.

- Choose an unsecured credit card if:

- You already have fair to excellent credit.

- You want higher credit limits and reward programs.

- You can qualify without needing to put down a deposit.

Building Credit Beyond Credit Cards with Ava Finance

While secured and unsecured credit cards are both valuable tools for credit building, they’re not the only option. For many people, pairing a credit card with a credit builder account provides faster and safer results.

That’s where Ava Finance comes in. Ava is a credit builder app designed to help you:

- Build positive payment history without high-interest debt.

- Save money while improving your credit score.

- Track your credit growth and financial progress over time.

Collections, past mistakes, or limited credit history don’t have to hold you back. By combining smart use of credit cards with Ava’s structured tools, you can take control of your credit report and move confidently toward financial stability.

Conclusion

Choosing between a secured and unsecured credit card comes down to where you are in your credit journey. Secured cards give beginners and rebuilders a reliable foundation, while unsecured cards reward those with stronger credit profiles. Both, however, require responsibility — making on-time payments, keeping balances low, and monitoring your credit report.

And remember, building credit isn’t just about cards. With Ava Finance, you can accelerate your journey by adding consistent positive payment history, saving money, and creating long-term financial stability. Your credit future doesn’t have to wait — you can start rebuilding today.