If your credit score isn’t where you want it to be, you’ve probably seen advice about credit repair or credit building. But these two strategies serve different purposes—and understanding the difference is key to choosing the right approach for your situation.

In this guide, you’ll learn:

- What credit repair is (and isn’t)

- What credit building means

- How both affect your credit score

- Red flags to avoid when using credit repair services

- How to repair your credit yourself

- Smart ways to build credit from scratch or after damage

- Why using Ava Finance, a credit builder app, is a smart move

What Is Credit Repair?

Credit repair is the process of identifying and correcting inaccurate, outdated, or fraudulent information on your credit report. The goal is to eliminate negative marks that don’t belong—errors that may be unfairly damaging your score.

What Credit Repair Does:

- Disputes errors with credit bureaus

- Removes incorrect or duplicate accounts

- Challenges outdated negative information

- Helps resolve identity theft-related issues

What It Doesn’t Do:

- It can’t remove legitimate negative marks (e.g., missed payments, charged-off accounts, bankruptcies)

- It doesn’t guarantee score improvement

- It won’t add new positive credit history

Tip: Credit repair is best when your report has inaccurate or suspicious items—not as a general method to increase your score.

What to Know About Credit Repair Companies

Many companies offer to repair your credit for a fee. While some are legitimate, many exploit consumers with false promises and illegal practices.

Legal Requirements Under the CROA (Credit Repair Organizations Act):

- They cannot charge you before services are performed

- They must provide a written contract outlining services, timeline, and costs

- You have a 3-day right to cancel with no charge

- They must explain your legal rights

Signs of a Credit Repair Scam:

- Promises to boost your credit score “guaranteed” or “instantly”

- Requests for payment upfront

- Advice to lie on applications or dispute accurate information

- Tells you not to contact credit bureaus yourself

- Offers to create a “new” credit identity

If a company does any of these, it’s a red flag. You can file a complaint with the FTC or your state attorney general.

How to Repair Credit Yourself (DIY Credit Repair)

If you're dealing with legitimate errors, you don’t need to pay someone else to fix them. The process is straightforward and can be done online.

Step-by-Step DIY Credit Repair:

- Get Your Credit Reports

- Access free reports at AnnualCreditReport.com

- Review reports from Equifax, Experian, and TransUnion

- Identify Inaccuracies

- Look for accounts you don’t recognize, incorrect balances, or outdated delinquencies

- File Disputes

Use each bureau’s online dispute center- Include supporting documentation (e.g., letters, statements, police reports for ID theft)

- Include supporting documentation (e.g., letters, statements, police reports for ID theft)

- Wait for Results

- Credit bureaus must investigate and respond within 30 to 45 days

- If the information is verified, it remains. If it can’t be confirmed, it must be removed

While this takes time, it’s completely free and just as effective as paying a third party.

What Is Credit Building?

While credit repair cleans up the past, credit building is about shaping a better financial future. It involves actions that add positive information to your credit report, which helps grow your credit score steadily over time.

Credit Building Activities:

- Making on-time payments

- Opening new accounts responsibly (secured cards, credit builder loans)

- Using credit without maxing out your cards

- Keeping old accounts open

- Diversifying your credit types (installment + revolving)

Credit building is essential for:

- Young adults with no credit history

- Anyone rebuilding after financial hardship

- Immigrants or new citizens with thin files

Bottom line: If your credit report is accurate but your score is still low, focus on credit building.

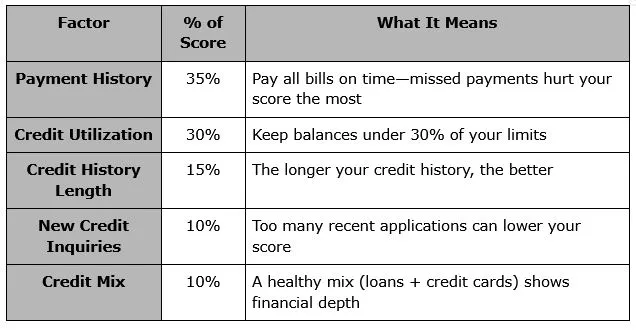

What Makes Up Your Credit Score?

Understanding the five key factors that impact your credit score helps you decide whether to focus on repair, building, or both.

Tools That Help You Build Credit

If you're starting from scratch or rebuilding, consider these options:

1. Secured Credit Cards

- Requires a refundable deposit

- Reports to all three credit bureaus

- Helps establish or rebuild payment history

2. Credit Builder Loans

- A small loan held in a locked savings account

- You make monthly payments; receive the funds after the loan term

- Builds payment history and savings at the same time

3. Authorized User Status

- Join a trusted person’s credit card as an authorized user

- Their history reflects on your report (as long as they pay on time)

4. Credit Building Apps Like Ava Finance

- Ava Finance is designed to help users build credit safely

- Makes small, manageable payments that are reported to credit bureaus

- Offers insights, credit tracking, and progress tools

These tools are especially helpful for people without traditional access to loans or credit cards.

Can You Use Credit Repair and Credit Building Together?

Yes—and often, using both is the most effective strategy.

Use Credit Repair When:

- There are errors or fraudulent accounts on your credit reports

- You’ve been a victim of identity theft

- You need to clean up old, inaccurate records before applying for a mortgage or loan

Use Credit Building When:

- Your credit file is thin or nonexistent

- You’ve paid off debts but need to boost your score

- You want to show lenders you're responsible over time

Combining both helps you remove roadblocks and build a stronger credit foundation simultaneously.

Why Ava Finance Is the Smart Way to Build Credit

If you’re looking for an accessible, no-stress way to build credit, Ava Finance is a top-tier option.

Ava Finance Offers:

- Credit-building plans with manageable payments

- Monthly credit bureau reporting to grow your credit score

- Educational insights tailored to your financial behavior

- No need for a large deposit like traditional secured cards

Unlike traditional credit cards or complex loans, Ava is designed for real people—whether you’re just getting started or getting back on track.

Think of Ava as your financial training wheels—helping you pedal toward better credit without the stress of falling over.

Final Thoughts: Build Credit, Don’t Just Repair It

Understanding the difference between credit repair and credit building helps you take the right action for your financial goals.

- Use credit repair to clear up inaccuracies

- Use credit building to add strength and stability to your report

- Combine both for the best results

And when you're ready to take that next step toward better credit, Ava Finance is your trusted partner. With easy-to-use tools, personalized credit tracking, and educational support, Ava empowers you to take control of your credit—on your terms.