Financial emergencies can strike when you least expect them. Whether it’s a medical bill, car repair, or unexpected travel, sometimes you just need access to cash—fast. A cash advance might seem like an easy solution, but before you withdraw money from your credit card, it’s essential to understand the long-term implications. In this guide, we’ll explain how cash advances work, how they may impact your credit score, the risks involved, and smarter ways to manage financial gaps while building credit history responsibly.

What Is a Cash Advance and How Does It Work?

It looks like an ATM withdrawal, but the cost is much higher. Do you know what you’re really signing up for when you take out a cash advance?

A cash advance is a short-term loan taken against your available credit card balance. Instead of using the card to make a purchase, you're withdrawing cash, typically from an ATM, bank, or using a convenience check issued by your credit card provider. Though it delivers quick cash, this transaction comes with high fees and interest rates.

Key Differences Between Purchases and Cash Advances:

- Credit Limit Access: Your cash advance limit is usually only a portion of your total credit limit.

- Transaction Fees: Most issuers charge 3% to 5% of the amount withdrawn or a flat fee—whichever is higher.

- Interest Rates: Cash advances generally come with much higher APRs than regular purchases and begin accruing interest immediately, without a grace period.

- Repayment Priority: Payments you make to your card may be applied to lower-interest balances first, allowing your high-interest cash advance balance to grow.

Understanding these terms is critical before proceeding with this form of borrowing. Unlike regular purchases, cash advances are one of the most expensive ways to use your credit card.

How Can a Cash Advance Affect Your Credit Score?

A cash advance doesn’t directly damage your score—but it can trigger a series of actions that do.

A single cash advance won’t automatically lower your credit score. However, the consequences of carrying a high balance and failing to pay it off promptly can indirectly harm your credit profile.

Here's How It Happens:

- Increased Credit Utilization: Your credit utilization ratio is the amount of credit you’re using compared to your limit. A large cash advance can spike your utilization and cause a score dip.

- Higher Minimum Payments: Because interest starts accruing immediately, your monthly payment obligation may increase, putting strain on your budget.

- Missed Payments: If your balance becomes unmanageable, you might miss a payment. A 30-day late payment can stay on your credit report for seven years and significantly drop your score.

- Difficulty Paying Down the Balance: Due to payment application policies, it might take longer to pay off a cash advance balance compared to regular purchases.

While the transaction itself isn’t flagged by credit scoring models, the way you manage it—and the downstream financial behavior it prompts—can affect your credit score negatively.

The Rise of Cash Advance Apps: Help or Harm?

Skip the fees, dodge the interest—are cash advance apps the safe solution they claim to be?

Cash advance apps like Earnin, Dave, and Brigit offer a modern alternative to traditional borrowing. They allow users to access small advances based on their expected paycheck—typically $25 to $750.

Key Features:

- No Credit Check: These apps don’t rely on your credit score, making them accessible for those with thin or poor credit files.

- Fast Access: While some transfers take a few days, many apps offer instant access for an additional fee.

- Fee Structures: Although interest isn’t charged, apps often suggest voluntary tips, charge monthly subscription fees, or apply express delivery costs.

While seemingly harmless, these apps don’t build credit, don’t report positive repayment behavior, and may lead to repeated borrowing cycles. Some users even report overdraft fees due to timing mismatches between advances and paychecks.

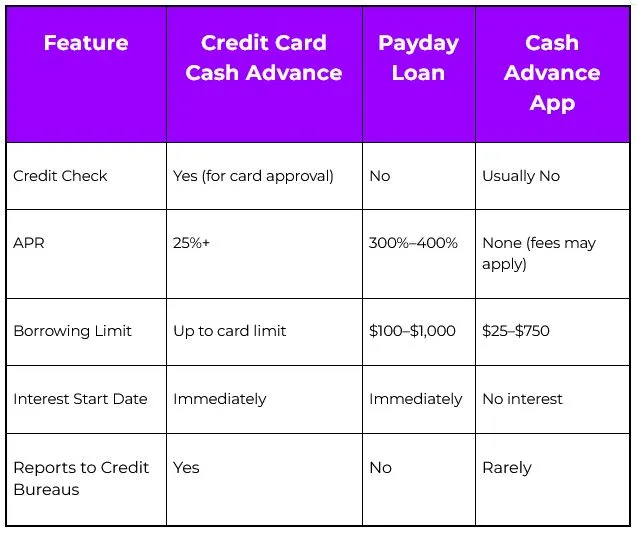

Comparing Cash Advances to Payday Loans and Cash Advance Apps

When money is tight, options feel limited—but not all short-term loans are created equal.

Cash advances, payday loans, and cash advance apps each serve the same purpose: to offer quick access to money. However, their terms, risks, and costs differ significantly.

Key Differences:

Payday loans carry the highest risk and the most predatory terms, often trapping borrowers in a cycle of debt. Compared to payday loans, a cash advance may be slightly less dangerous but still expensive. Apps may be more affordable in the short term, but they don’t improve your creditworthiness.

Safer Alternatives to Cash Advances

Before you borrow, know your options. Here are better ways to bridge a cash gap while protecting your credit.

1. Personal Loans

If your credit is in decent shape, a personal loan can be a cost-effective alternative. These loans offer predictable payments, fixed interest rates, and potentially lower APRs than cash advances. Some online lenders approve applications quickly, even offering next-day funding.

2. Credit Card Purchases (Instead of Advances)

If you don’t need physical cash, consider using your credit card for purchases instead. Regular transactions may come with a grace period and lower APRs.

3. Borrowing from Friends or Family

While this comes with emotional risk, borrowing from someone you trust may offer lower or no interest. Be transparent, formalize the agreement in writing, and set up a repayment plan.

4. Home Equity Options

If you own your home, a HELOC or home equity loan could provide access to larger sums at lower rates. However, your home becomes collateral, so the risk is higher.

5. Payday Alternative Loans (PALs)

Some federal credit unions offer PALs for amounts between $200 to $1,000. With interest rates capped at 28% and repayment terms of up to six months, these loans are regulated, transparent, and more affordable than payday loans.

Evaluating your short-term needs against long-term credit impact helps ensure you make the wisest borrowing choice.

Credit Building: A Better Long-Term Strategy

What if your financial emergencies became less frequent? That’s the power of building strong credit.

Rather than borrowing your way out of every emergency, build a solid credit foundation that helps you qualify for better financial tools over time. Responsible credit behavior—on-time payments, low balances, and account variety—leads to improved credit scores and opens up more favorable loan and credit options.

One of the easiest ways to start is by using tools designed specifically for credit building. That’s where Ava Finance comes in.

How Ava Finance Helps You Build Credit Smarter

Instead of borrowing at high rates, what if you could build credit without added debt?

Ava Finance is a credit builder app that allows you to grow your credit history through responsible, low-risk activity. Unlike cash advances, Ava doesn’t involve interest charges, deposits, or revolving debt.

Here’s how it works:

- Ava reports your payment activity to all three major credit bureaus.

- There are no interest charges or revolving balances.

- You develop healthy credit habits while maintaining financial control.

By using Ava, you can steadily improve your credit profile without taking on risky loans or high-fee financial products. It’s an ideal tool for those who want to build long-term financial stability without relying on emergency cash options.

Final Thoughts: Short-Term Cash vs. Long-Term Credit Health

Cash advances may seem like an easy fix in times of stress, but their long-term impact can create even more financial strain. From high interest rates to indirect credit score damage, the true cost often outweighs the benefit.

Instead of risking your credit health, explore safer, more strategic alternatives. Whether it’s a personal loan, a PAL, or building a stronger credit foundation through Ava Finance, you have options that won’t compromise your future.

Want to take control of your credit journey?

Start building smarter today with Ava Finance at www.meetava.com.

.webp)